Entity can account for its inventory by using either perpetual method or periodic method.

Under perpetual method:

- the entity record for every single movement of the inventory (i.e. in and out of the inventory)

- at any single point of time, the entity is able to recall the inventory on hand

- frequency of stock-take required is lesser than those accounted using periodic method

Under periodic method,

- every single movement for the inventory (i.e. in and out) is not required to be tracked

- the entity perform a periodic stock-take to ascertain the inventory balance

- inventory on hand can only be recalled after the stock-take is performed

- frequency of stock-take required is higher than those accounted using perpetual method

- cost of sales is computed by using the following formula: Opening Stock+ Cost of Goods Manufactured / Purchase - Closing stock

The above summarize the difference between perpetual inventory method and periodic inventory method.

Ernst & Young sued over Lehman's collapse

Here is the big news that might trigger your interest as an auditor.

One of the Big 4 accounting firms, Ernst & Young is facing a civil lawsuit in the US over the collapse of Lehman Brothers! New York's state attorney Andrew Cumo claims that New York's state attorney Andrew Cuomo claims Ernst & Young "sat by silently" as Lehman Brothers tried to conceal billions of dollars in debt from investors before its implosion. The lawsuit says Lehman ran a "massive accounting fraud".

It is claimed that Ernst & Young approved of Lehman's increasingly frequent use of a device known as Repo 105. The lawsuit alleges: "These Repo 105 transactions had no independent business purpose and were designed solely to enable Lehman to manage the company's financial balance sheet metrics."

The case centres on Lehman's use of an accountancy practice known as Repo 105, which involves temporarily removing money from the balance sheet to give the impression of greater financial strength. Mr Cuomo mentioned that, Ernst & Young should not have approved the accounts, knowing that the practice had been used so widely.

The lawsuit seeks more than $150 million in fees that Ernst & Young received from 2001 to 2008 as Lehman's outside auditor,plus other unspecified damages

Ernst & Young has responded, and claims that the firm is going to "vigorously defend" the lawsuit.

One of the Big 4 accounting firms, Ernst & Young is facing a civil lawsuit in the US over the collapse of Lehman Brothers! New York's state attorney Andrew Cumo claims that New York's state attorney Andrew Cuomo claims Ernst & Young "sat by silently" as Lehman Brothers tried to conceal billions of dollars in debt from investors before its implosion. The lawsuit says Lehman ran a "massive accounting fraud".

It is claimed that Ernst & Young approved of Lehman's increasingly frequent use of a device known as Repo 105. The lawsuit alleges: "These Repo 105 transactions had no independent business purpose and were designed solely to enable Lehman to manage the company's financial balance sheet metrics."

The case centres on Lehman's use of an accountancy practice known as Repo 105, which involves temporarily removing money from the balance sheet to give the impression of greater financial strength. Mr Cuomo mentioned that, Ernst & Young should not have approved the accounts, knowing that the practice had been used so widely.

The lawsuit seeks more than $150 million in fees that Ernst & Young received from 2001 to 2008 as Lehman's outside auditor,plus other unspecified damages

Ernst & Young has responded, and claims that the firm is going to "vigorously defend" the lawsuit.

#98- Expectation on FY 2010 inventory level

For audit of year-end 2010 audit, auditors should form an expectations that inventory level has reduced, as compared to previous year. Inventory level can be computed as inventory as % of sales / inventory as % of last 3 month sales. This provide a good guide / benchmark on the inventory level our audit clients are holding.

In view of the recovering business/ economy, inventory turnover are expected to become relatively quicker than prior year. Aged inventory are expected become relatively lesser either.

If the inventory level, as well as aged inventory level, remain relatively constatnt as prior year, this could indicate higher risk of provision for inventory obsolescence. Auditor should discuss this issue with management.

In view of the recovering business/ economy, inventory turnover are expected to become relatively quicker than prior year. Aged inventory are expected become relatively lesser either.

If the inventory level, as well as aged inventory level, remain relatively constatnt as prior year, this could indicate higher risk of provision for inventory obsolescence. Auditor should discuss this issue with management.

#97- Excess inventory after christmas

We were reading one of the business article online on how to deal with the excess inventory after the christmas sales, especially for retailers.

One of the options suggested was to auction it off online. Companies tend to store higher level of inventory during Christmas season, to meet the demand from customers. Demand from customers are often hard to be projected. Neither historical trend, nor forecast can precisely predict the inventory required. Hence, instead of losing sales resulted from insufficient inventory,Companies tend to store higher level of inventory to meet the demand from customers.

After Christmas sales, Companies are required to reduce the relatively high level (if any) of inventory, considering that the warehouse costs/ inventory holding costs/ liquidity costs could be substantial.

One of the options suggested was to auction the inventories off online. Though the pricing might not be attractive, but auctioning off the inventories allow the Companies to reduce all type of costs mentioned above.

Companies could sell the stocks in all sorts of website, including: e-bay.

One of the options suggested was to auction it off online. Companies tend to store higher level of inventory during Christmas season, to meet the demand from customers. Demand from customers are often hard to be projected. Neither historical trend, nor forecast can precisely predict the inventory required. Hence, instead of losing sales resulted from insufficient inventory,Companies tend to store higher level of inventory to meet the demand from customers.

After Christmas sales, Companies are required to reduce the relatively high level (if any) of inventory, considering that the warehouse costs/ inventory holding costs/ liquidity costs could be substantial.

One of the options suggested was to auction the inventories off online. Though the pricing might not be attractive, but auctioning off the inventories allow the Companies to reduce all type of costs mentioned above.

Companies could sell the stocks in all sorts of website, including: e-bay.

Impact on Accounting Education

Accounting is considered to be the language of business. The number of globalized businesses in the world is vast and increasing, which emphasizes the importance of achieving a common accounting language. Accounting is predominantly known as the profession that analyzes the past, but because of globalization it is important to look into the future.

As a result, it is important to educate the accounting field on the standards of other countries. The IRSF was created by the International Accounting Standards board. The Financial Accounting Standards Board created the generally accepted accounting principles.

Accounting is predominantly known as the profession that analyzes the past and looks into the future. Globalization plays a huge role on accounting education. Thus it is more important to educate accountants on the standards of other countries, so that they are knowledgeable in their field because many businesses operate with countries across the world.

The accounting education is more important in such a way that the accountant becomes a part of the management and decision-making team, rather than just providing the financial information. Accounting in the future will require not only specific knowledge but also must also be able to change with the globalization. Accountants will need to be well prepared in computer skills, the ability to learn new software and new accounting rules.

Realizing the importance of information technology most of the colleges and universities have added a new track called Accounting Information System. The Professional accountants employ extensively in the computer applications to perform their tasks such as email to communicate, Internet for search, and accounting software to record and analyze financial transactions for decision-making. Computerized accounting systems have now replaced manual accounting systems in most of the organizations.

Significance of Accounting Payroll

Payroll Accounting is important for an Employee and the Employer, which deals with the payment of your employees and paying the appropriate taxes to the government. The payroll system is the most frequently updated part of financial record in most of the organizations. Nowadays even a small business can manage this system with the online processing sites.

Payrolls are considered to be the lifeline of any organization. It consists of procedures and mechanisms ensuring that an accountant processes the employee salary information in complete manner with accuracy. Also allows the business owners to create a function that is easy for them to understand and use. Usually small businesses run their payroll systems like that of the larger organizations.

In many organizations there are several pension plans, offered to their previous employees based on the duration and the importance of their responsibilities. It is very important for an organization to maintain and manage their payrolls. If the payrolls are kept by the organization in an efficient manner, it would keep the employees, in the healthiest state of mind.

If there is any occurrence of issues in the payrolls of the company, then it may lead to the employee dissatisfaction having a direct bearing on the efficiency of their services. Thus the Payroll accountant has to take care of the payrolls right from the salaries and wages such as paid vacation, insurance coverage of the company. They must properly integrate the pay records with the payroll and the benefit systems.

A manual payroll system requires that the payroll to be processed by hand and is therefore a considerably slower procedure. But an automated payroll system enables the employer to process its payroll through a computerized system which makes the process faster by reducing the errors that occurs in manual system. This may be considered as one of the demerit that the employer must invest in for the payroll software and maintain it.

Accounting principle- Accrual Basis

Figures generated / kept in accordance to accounting principle is prepared on accrual basis. For instance, accountant record the provision for warranty ( based on estimate) even though there's no actual cash/ economic outflow yet.

In finance, cash basis figures are more relatively more valuable , as compared to accrual basis ( advocated by accounting principle), in order to value a business.

What do you think ? You prefer a an accrual method or cash method in valuing a business?

In finance, cash basis figures are more relatively more valuable , as compared to accrual basis ( advocated by accounting principle), in order to value a business.

What do you think ? You prefer a an accrual method or cash method in valuing a business?

Auditing Creditors- Creditor Turnover Analysis

In audit, it's essential to form an expectation of the Company's results before we really drill into the details. We compare the actual Company's results to our expectation, and investigate the variances accordingly. This is the analytical procedures adopted by most of the audit Company. Besides, we also compare the result / financial position with prior period.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

Creditors' turnover anlaysis is one of the auditing procedure we performed. What are we expecting from the audit client, in general. We expect the creditors turnover (days) to increase, as compared to prior period.

To illustrate, majority of our audit clients are affected by the economy turmoil. They are squeezing suppliers' credit ( by delyaing the repayment), in order to maintain the Company's working capital, as our audit client's working capital are most likely affected by the delay of repayment from customers.

We have formed an expectation, and we will compare the actual result with our expectation. Any unusual movements need to be identified.

Auditing: Annual Budget vs Actual Results

Company prepare budget and use budget as a performance benchmark and monitoring tools. For instance, senior management can question sales department if their actual yeat-to-date entertainment has exceeded the budget before the end of the year. Budget is , usually, prepared and approved at the beginning of the year or before that.

Budget has incorporated management's forecast, estimation and outlook of the business in the coming times.

Is management's budget useful to auditor?

The answer is yes. Budget, which represents management's expectation, should be compared against the actual results. Significant variances should be investigated. Apparently, management would have to explain the variances. It's important for auditor to find out the reason of the variances to identify potential changes in business operation, significant developments during the year.

Understanding how management view the business (by looking at the budget) is a crucial stage in audit planning, it enhance our knowledge and understanding on the business, the industry and the overall economy as a whole.

Budget has incorporated management's forecast, estimation and outlook of the business in the coming times.

Is management's budget useful to auditor?

The answer is yes. Budget, which represents management's expectation, should be compared against the actual results. Significant variances should be investigated. Apparently, management would have to explain the variances. It's important for auditor to find out the reason of the variances to identify potential changes in business operation, significant developments during the year.

Understanding how management view the business (by looking at the budget) is a crucial stage in audit planning, it enhance our knowledge and understanding on the business, the industry and the overall economy as a whole.

Disposing capital-intensive business

What's happening in the corporate world now?

Capital-intensive require heavy investment of resources, including, but not limimted to: cash, human resource,management's effort, etc. As part of the restructuring exercise to scale down, there are evidence that a lot of corporate are disposing off capital-intensive business.

How would disposing capital-intensive business benefit the corporate?

- immediate liquidity ( i.e. proceeds from disposal)

- better working capital management

- allow management to evaluate other business opportunities

- lesser resources are required, which allow the business to scale down

- higher return on asset ("ROA") ratio

However, it's always not easy to dispose off a capital-intensive business unit/ busines during this business environment, unless a substantial discount is given to the potential buyers.

Capital-intensive require heavy investment of resources, including, but not limimted to: cash, human resource,management's effort, etc. As part of the restructuring exercise to scale down, there are evidence that a lot of corporate are disposing off capital-intensive business.

How would disposing capital-intensive business benefit the corporate?

- immediate liquidity ( i.e. proceeds from disposal)

- better working capital management

- allow management to evaluate other business opportunities

- lesser resources are required, which allow the business to scale down

- higher return on asset ("ROA") ratio

However, it's always not easy to dispose off a capital-intensive business unit/ busines during this business environment, unless a substantial discount is given to the potential buyers.

Accounting treatment for tax penalty

One of our Accounting & Audiitng blog reader inquired us the following:

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

No depreciation charge on asset held for sale

This is to confirm that if a property is classified as asset held for sale, no depreciation is to be recorded.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

Auditing Creditors

One of the procedures required to audit trade creditors account is to audit the creditors' statement received from the audit client's suppliers (i.e. external audit evidence).

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

Cash audit- internal controls in cash process- cash payment

In our earlies entries in relation to cash audit, we discussed about the audit procedures of auditing unpresented cheques. We will discuss more extensively for audit procedures in auditing cash and bank balances of our audit clients.

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details

The Types Of Accounting

Accounting is the art of analyzing and interpreting data. It may not be apparent to some but every business and every individual uses accounting in some form. An individual may knowingly or unknowingly use accounting when he evaluates his financial information and relays the results to others. Accounting is an indispensable tool in any business, may it be small or multi-national.

The term "accounting" covers many different types of accounting on the basis of the group or groups served. The following are the types of accounting.

1. Private or Industrial Accounting: This type of accounting refers to accounting activity that is limited only to a single firm. A private accountant provides his skills and services to a single employer and receives salary on an employer-employee basis. The term private is applied to the accountant and the accounting service he renders. The term is used when an employer-employee type of relationship exists even though the employer is some case is a public corporation.

2. Public Accounting: Public accounting refers to the accounting service offered by a public accountant to the general public. When a practitioner-client relationship exists, the accountant is referred to as a public accountant. Public accounting is considered to be more professional than private accounting. Both certified and non certified public accountants can provide public accounting services. Certified accountants can be single practitioners or by partnership ranging in size from two to hundreds of members. The scope of these accounting firms can include local, national and international clientele.

3. Governmental Accounting: Governmental accounting refers to accounting for a branch or unit of government at any level, may it be federal, state, or local. Governmental accounting is very similar to conventional accounting methods. Both the governmental and conventional accounting methods use the double-entry system of accounting and journals and ledgers. The object of government accounting units is to give service rather than make profits. Since profit motive cannot be used as a measure of efficiency in government units, other control measures must be developed. To enhance control, special funds accounting is used. Governmental units can use the services of both private and public accountant just as any business entity.

4. Fiduciary Accounting: Fiduciary accounting lies in the notion of trust. This type of accounting is done by a trustee, administrator, executor, or anyone in a position of trust. His work is to keep the records and prepares the reports. This may be authorized by or under the jurisdiction of a court of law. The fiduciary accountant should seek out and control all property subject to the estate or trust. The concept of proprietorship that is common in the usual types of accounting is non-existent or greatly modified in fiduciary accounting.

5. National Income Accounting: National income accounting uses the economic or social concept in establishing accounting rather than the usual business entity concept. The national income accounting is responsible in providing the public an estimate of the nation's annual purchasing power. The GNP or the gross national product is a related term, which refers to the total market value of all the goods and services produced by a country within a given period of time, usually a calendar year.

Pursuing a Career in Accounting? Opportunities Are Yours For the Taking

If you're interested in pursuing a career in accounting or auditing, the opportunities may be yours for the taking. According to the Bureau of Labor Statistics' Occupational Outlook Handbook, 2008-09 Edition, the accounting profession will experience strong job growth over the period from 2006 to 2016. Accounting jobs are expected to grow by 18 percent between 2006 and 2016. This growth is faster than the average for all occupations. It is projected that almost 226,000 accounting jobs will be created during the ten year period. The strong growth in accounting and auditing jobs is expected to result from economic expansion, changes to financial laws, and stricter corporate governance. Accounting career opportunities will also be created by changes to financial reporting standards, business investments, mergers and acquisitions, and other events that are expected to lead to greater scrutiny of accounting practices and company finances. Growth in accounting jobs will also be driven by the desire to make government agencies more accountable. According to the Handbook, candidates with a master's degree, who obtain certification or licensure, or who are skilled at using accounting and auditing computer software will have the best career opportunities.

What jobs do accountants and auditors do? The role of accountants and auditors is quite broad. Generally speaking, accountants and auditors prepare, analyze, verify and communicate financial information for clients that may include corporations, governments, non-profit organizations, or individuals. But the specific job descriptions of accountants and auditors vary depending on the type of accounting and auditing job.

What types of accounting career opportunities are there? There are four major fields of accounting and auditing: public, management, government accounting, and internal auditing.

Public accounting jobs: Public Accountants provide a wide range of consulting services relating to accounting, auditing, tax, and other financial activities. A career in a public accounting involves providing services such giving advice to companies or individuals to help them get certain tax advantages and preparing and filing income tax returns. External auditors are responsible for auditing financial statements for companies to ensure that they have been prepared properly. Many public accountants have the professional designation Certified Public Accountant (CPA) and they may work on their own or in public accounting firms.

Management accounting jobs: Management accountants prepare and analyze the financial information of the companies for which they work. If you pursued a career in management accounting, you would be responsible for maintaining budgets, managing expenses, analyzing financial information, preparing financial reports and managing company assets.

Government accounting jobs: A career in government accounting means you would be employed by a Federal, State, or local government agency. Government accountants are responsible for maintaining and analyzing the financial records of these agencies. They may also be responsible for auditing private businesses and individuals. For example, accountants for the Internal Revenue Service are employed by the federal government to review taxes received by businesses and individuals. In addition, they are tasked with the responsibility of ensuring that the various government agencies are making expenditures in accordance with applicable laws and regulations.

Internal auditing jobs: Internal auditors are responsible for ensuring that the financial records of a company or individual are accurate. They check for fraud or non-compliance with laws, and they help to prevent financial loss. Other responsibilities of an internal auditor may include reporting on audits, advising on or recommending changes to a company's operations an/or financial activities, reviewing data regarding a company's assets, liabilities, stock, income and expenditures, preparing reports and financial statements, and reviewing compliance with corporate policies and government regulations.

What are the educational requirements for a career in accounting or auditing? Your duties as an accountant will vary according to what type of accounting you decide to specialize in or what kind of accounting job you want to pursue. Accordingly, if you are pursuing career opportunities in accounting or auditing, the education and training requirements can vary depending on your role. Most accounting jobs require at least a bachelor's degree in accounting or a related field but some employers will only consider job applicants with a master's degree in accounting, or a master's degree in business administration with a concentration in accounting.

Licensure and certification for accounting jobs: Only a Certified Public Accountant is permitted to file reports with the Securities and Exchange Commission (SEC). Accordingly, if you're interested in a career working for a public company that's registered with the SEC, you need to be licensed as a CPA by your State Board of Accountancy. Most States require CPA candidates to be college graduates and to have some accounting experience. To become a CPA, you must pass a four-part examination prepared by the American Institute of Certified Public Accountants (AICPA). This is required by all States.

Things that can help increase your accounting career opportunities:

o Previous experience in accounting or auditing, such as experience gained in summer or part-time internship programs, will help your chances of getting an accounting job.

o Knowledge of computers and financial software applications will make you a stronger candidate for an accounting job.

o Previous experience in accounting or auditing, such as experience gained in summer or part-time internship programs, will help your chances of getting an accounting job.

o Knowledge of computers and financial software applications will make you a stronger candidate for an accounting job.

What skills do you need to succeed in an accounting career? If you're interested in accounting career opportunities, you must:

o be proficient in math and you must have excellent analytical skills

o communicate effectively

o be good at working with people

o have basic accounting knowledge

o be familiar with accounting software

o be proficient in math and you must have excellent analytical skills

o communicate effectively

o be good at working with people

o have basic accounting knowledge

o be familiar with accounting software

If you're seriously thinking about accounting or auditing career opportunities, information is available from the following organizations:

o AACSB International

o American Institute of Certified Public Accountants

o National Association of State Boards of Accountancy

o Institute of Management Accountants

o Accreditation Council for Accountancy and Taxation

o The Institute of Internal Auditors

o ISACA

o Association of Government Accountants

o American Institute of Certified Public Accountants

o National Association of State Boards of Accountancy

o Institute of Management Accountants

o Accreditation Council for Accountancy and Taxation

o The Institute of Internal Auditors

o ISACA

o Association of Government Accountants

Should I Practice Public Or Private Accounting

Bachelor of Science in Accountancy is one of the picked courses among college students. Many have chosen this field of study because it has a wide scope of availability in terms of future stable job with attach high rate of pay. Career opportunities in this course have two categories and these are Public and Private Accounting.

Professionals who worked for a particular Accounting Firm and worked for several clients are called Public Accountants. These kind of firms employ thousands of accountants because their services are offered from one-person operations to multinational organizations. Audit or tax is two paths where in a Public accountant is going to be. Auditors as you called for those in the audit practice strictly and carefully audit financial records and business transactions of a client. Accounting records that are reported by the companies are ensured by the auditors that those documents accurately abide with national accounting standards. Professionals who are in the tax practice provide services similar with that of an auditor but with a more focus specialization. Professionals who handles tax ensures that clients tax record are well documented and do follow the guidelines established by government taxing policies. Another role of a tax accountant is to help minimize the tax liability of a client.

On the other hand Private Accounting is more concern with internal accounting. This internal accounting is the accounting functions of the company. Corporate Accountants which is another name for private accountant performs the same duties as the Public accountant but this task are limited towards the companies that they are employed.

The distinction between Public and private Accounting is that Public is more involved with collecting external financial information's while Private is much inclined with the use of internal information's to aid managers in giving effective decisions.

#96- Cash audit- internal controls in cash process- cash payment

In our earlies entries in relation to cash audit, we discussed about the audit procedures of auditing unpresented cheques. We will discuss more extensively for audit procedures in auditing cash and bank balances of our audit clients.

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details (e.g suppliers' invoices), etc

Auditors may consider test the internal controls of the client's cash process. For this entry, we will provide an overview of the possible audit procedures to test the internal controls in cash payment process:

(a) select certain number of random samples, and test that payment voucher are properly prepared and authorised

(b) select certain number of random samples, and test that bank reconciliations are properly prepared and reviewed

(c) select certain number of random samples, and test that journal entries are properly posted into General Ledger

(d) select certain number of random samples, and test that payment voucher details match with the corresponding payment details (e.g suppliers' invoices), etc

#95- Auditing Creditors IV

In previous posts in relation to auditing creditors, we mentioned about:

- Review of Creditors' Statement of Account

- Purchase Cut-off testing

- Comparison of current year balance to prior year balance

In addition to the above, it would be good if a creditors' turnover analysis is performed:

Creditors Turnover (day): Purchase/ Average Trade Creditors x 365 [for periodic inventory system]

Creditors Turnover (day): Purchase/ Average Trade Creditors x 365 [for perpetual inventory system]

Auditor can compare the creditors' turnover (day) computed above to general creditor term given by the creditors to assess if the Company has been repaying on time. If the creditors' turnover (day) is significantly longer than the credit term given by suppliers, this might indicate the liquidity issue the Company is facing.

- Review of Creditors' Statement of Account

- Purchase Cut-off testing

- Comparison of current year balance to prior year balance

In addition to the above, it would be good if a creditors' turnover analysis is performed:

Creditors Turnover (day): Purchase/ Average Trade Creditors x 365 [for periodic inventory system]

Creditors Turnover (day): Purchase/ Average Trade Creditors x 365 [for perpetual inventory system]

Auditor can compare the creditors' turnover (day) computed above to general creditor term given by the creditors to assess if the Company has been repaying on time. If the creditors' turnover (day) is significantly longer than the credit term given by suppliers, this might indicate the liquidity issue the Company is facing.

#94- Auditing Creditors III

In our previous entries in relation to auditing creditors and auditing creditors II, we discussed about the audit procedures for trade creditors balances:

(i) Review of Creditors' Statement of Account

(ii)Purchase cut-off testing [ Please also refer to interesting comments posted by our readers

Apart from the procedures mentioned above, auditor should also perform analytical review, by comparing current year creditors' balance to prior year creditors' balance to investigate if there's any unusual fluctuations or absence of expected fluctuations.

For instance, sales volume for ABC company reduced substantially during the year, while the trade creditors balance has increased significantly. We need to understand / analyse the reasons caused the increase in trade creditors' balance while the sales volume has dropped substantially. One of the possible answer is due to the ABC Company is having liquidity issue, and resulted in delaying in repaying its trade creditors.

A good and thorough analytical review give auditor a better understanding of the business.

(i) Review of Creditors' Statement of Account

(ii)Purchase cut-off testing [ Please also refer to interesting comments posted by our readers

Apart from the procedures mentioned above, auditor should also perform analytical review, by comparing current year creditors' balance to prior year creditors' balance to investigate if there's any unusual fluctuations or absence of expected fluctuations.

For instance, sales volume for ABC company reduced substantially during the year, while the trade creditors balance has increased significantly. We need to understand / analyse the reasons caused the increase in trade creditors' balance while the sales volume has dropped substantially. One of the possible answer is due to the ABC Company is having liquidity issue, and resulted in delaying in repaying its trade creditors.

A good and thorough analytical review give auditor a better understanding of the business.

Closing of Account in Numia

Numia provides you a way to close your account by retrieving all your accounting transactions. Closing of your accounts prevents you from logging in and to access any of the services provided by Numia. The steps followed in closing of account in Numia are

1) Select Company -> Close Numia Account.

2) A new window will be opened similar to the screenshot as below.

3) By clicking the "Close Account" Button, Your account will be closed.

3) By clicking the "Close Account" Button, Your account will be closed.

As soon as you closed your account, You are not logged out immediately. You may manage your accounts even now too and it will be audited as before.

If you want to reactivate your account with Numia, You will be given a period of 48 hours or 2 days (from the time you closed your account) to login again. You or the persons linked with this account can login to the website within this stipulated period of time to activate your account.

After the deadline given by Numia to reactive your account is completed, Your account will be permanently closed. You can contact support@numia.biz for retrieval of your accounting records or any kind of assistance.

1) Select Company -> Close Numia Account.

2) A new window will be opened similar to the screenshot as below.

3) By clicking the "Close Account" Button, Your account will be closed.

3) By clicking the "Close Account" Button, Your account will be closed.As soon as you closed your account, You are not logged out immediately. You may manage your accounts even now too and it will be audited as before.

If you want to reactivate your account with Numia, You will be given a period of 48 hours or 2 days (from the time you closed your account) to login again. You or the persons linked with this account can login to the website within this stipulated period of time to activate your account.

After the deadline given by Numia to reactive your account is completed, Your account will be permanently closed. You can contact support@numia.biz for retrieval of your accounting records or any kind of assistance.

Banking Registers

Register is basically the official written record of names or events or transactions. Banking Registers are the records which are maintained in order to keep track of your banking transactions.

Numia, online accounting software not only helps you to record your accounting transactions or maintain your banking records, but also enables you to edit or delete the transaction. You can view the report of the transactions each and every bank separately within your desired time period.

The steps involved are as follows:

• Select Bank-> Banking Registers.

• Select the bank name to view the accounting transactions in that specified bank.

• Select the account name.

• Now you can view the list of transactions made in that bank in the corresponding account name.

• Edit or delete the transaction by just clicking the edit or delete icons which is viewed by moving the cursor over the transaction.

• You can also customize the report by clicking “Customize” option. Customizing allows you to view the transaction report within specified dates and to differentiate the transactions based on reconciliation.

• You can also export the report to “Excel spreadsheet” or simply print it.

Numia, online accounting software not only helps you to record your accounting transactions or maintain your banking records, but also enables you to edit or delete the transaction. You can view the report of the transactions each and every bank separately within your desired time period.

The steps involved are as follows:

• Select Bank-> Banking Registers.

• Select the bank name to view the accounting transactions in that specified bank.

• Select the account name.

• Now you can view the list of transactions made in that bank in the corresponding account name.

• Edit or delete the transaction by just clicking the edit or delete icons which is viewed by moving the cursor over the transaction.

• You can also customize the report by clicking “Customize” option. Customizing allows you to view the transaction report within specified dates and to differentiate the transactions based on reconciliation.

• You can also export the report to “Excel spreadsheet” or simply print it.

Exporting your Report to Excel Spreadsheet

In Numia, You can easily export your report to excel spreadsheet. By exporting your report, You may be able to save the report under any name in your desired path and you can make whatever changes you want to do. The steps involved are given below:

1.Select Report -> Choose the report you want to export.

2.Click “Excel Spreadsheet” Button.

3.Choose “Save file”.

4.Select the folder where you want to save the file. You can also change the name of the file.

5.Open the file in excel and make the changes you want. This change does not affect the data in the Numia reports.

The screenshot is as follows.

1.Select Report -> Choose the report you want to export.

2.Click “Excel Spreadsheet” Button.

3.Choose “Save file”.

4.Select the folder where you want to save the file. You can also change the name of the file.

5.Open the file in excel and make the changes you want. This change does not affect the data in the Numia reports.

The screenshot is as follows.

Ebay Transactions :

Ebay is an American internet firm which acts as a world’s online marketplace. It manages a website, ebay.com which is the place where buyers and sellers come together and trade goods, services and almost everything. Ebay has been started in 1995 and it is now multi-billion dollar business comprised over thirty countries.

The basic working of Ebay includes two factors such as Bidding and Buy it now.

•A seller can list any kind of item like antiques, cars, books, sporting good and almost everything on Ebay.

•The seller has to decide whether he prefers bidding by accepting bids on the item or he may choose buy it now option to make the buyers to buy the item right away at a fixed price.

•In the bidding method, the auction is opened by the seller for some price and it remains in ebay for certain number of days. Then, the buyers are allowed to place the bids on the item. When the specific period ends, the buyer with the highest bid will win.

•In Buy it now option, the buyer who accepts the seller’s price at first gets the item.

Numia, the online accounting software is making lots of improvements with simpler accounting modules, each aiming to make this accounting software better and easier to use. In the path of development, Numia’s future plan is to include the access to Ebay transactions to make the accounting processes in a effective manner.

The basic working of Ebay includes two factors such as Bidding and Buy it now.

•A seller can list any kind of item like antiques, cars, books, sporting good and almost everything on Ebay.

•The seller has to decide whether he prefers bidding by accepting bids on the item or he may choose buy it now option to make the buyers to buy the item right away at a fixed price.

•In the bidding method, the auction is opened by the seller for some price and it remains in ebay for certain number of days. Then, the buyers are allowed to place the bids on the item. When the specific period ends, the buyer with the highest bid will win.

•In Buy it now option, the buyer who accepts the seller’s price at first gets the item.

Numia, the online accounting software is making lots of improvements with simpler accounting modules, each aiming to make this accounting software better and easier to use. In the path of development, Numia’s future plan is to include the access to Ebay transactions to make the accounting processes in a effective manner.

Sending Report Through Email

Reports act as a document for viewing all of your transactions in a same place. They are the formal account of the proceedings or transactions of a group. The basic purpose of reports is to inform, in terms of a written document featured with informations.

Numia provides a simple way of sending any report to multiple email ids in a easier way. The steps involved are as follows.

• Select Reports -> click the report you want to get emailed.

• Click "Email" option.

• Email form will be shown.

• Enter the email address to which the report has to be send.

• You can also enter the message, if you wish the report to be sent with the message.

• Then by clicking "Send Report", Your report will be sent.

Numia provides a simple way of sending any report to multiple email ids in a easier way. The steps involved are as follows.

• Select Reports -> click the report you want to get emailed.

• Click "Email" option.

• Email form will be shown.

• Enter the email address to which the report has to be send.

• You can also enter the message, if you wish the report to be sent with the message.

• Then by clicking "Send Report", Your report will be sent.

#93- Auditing Creditors II

In addition, we should perform purchase cut-off test to address the potential risk of misstatement arising from improper cut-off.

As an auditor, we can examine the Goods Received Notes ("GRN") near year-end and after year-end to check that Goods Received Notes details matached with the supplier's delivery order details and supplier's invoices details.

For instance, Auditor Arthur is auditing Company E (whose year end is 30 June 2010) creditor's balance. As part of cut-off testing procedure, Auditor Arthur requested the details of Goods Received Notes near year-end and after year-end. And noted the following sample:

"Goods received notes was generated on 01 July 2010, however, supplier's invoices, supplier's DO indicated the date of 30 June 2010. Further investigation revealed that, supplier generated their internal documents on 30 June 2010, but only delivered the goods to Company E in 01 July 2010. As such, there's no exceptions for Company E"

Cut-off testing is deemed as a compulsory procedure in auditing creditors' balances.

As an auditor, we can examine the Goods Received Notes ("GRN") near year-end and after year-end to check that Goods Received Notes details matached with the supplier's delivery order details and supplier's invoices details.

For instance, Auditor Arthur is auditing Company E (whose year end is 30 June 2010) creditor's balance. As part of cut-off testing procedure, Auditor Arthur requested the details of Goods Received Notes near year-end and after year-end. And noted the following sample:

"Goods received notes was generated on 01 July 2010, however, supplier's invoices, supplier's DO indicated the date of 30 June 2010. Further investigation revealed that, supplier generated their internal documents on 30 June 2010, but only delivered the goods to Company E in 01 July 2010. As such, there's no exceptions for Company E"

Cut-off testing is deemed as a compulsory procedure in auditing creditors' balances.

Memorized Reports

Reports are often used to display the result of an experiment, investigation, or inquiry. Memorized reports help you to memorize the important reports and make it easy to view.

Numia provides a better way to memorize your reports to have them for future reference. By memorizing, it gets saved automatically in the Memorized Report List. Then, when you want to create a similar report, you can go to the Memorized Report List to find it.

The steps involved in memorizing a report are

* Click Reports -> Select the specific report you want to memorize

* Click the "Memorize" Button.

* Enter the title under which the specified report is going to be memorized

* By clicking Memorize button, the report will be saved.

* You can view, edit or delete the memorized report by selecting Report -> Memorized Reports.

Numia provides a better way to memorize your reports to have them for future reference. By memorizing, it gets saved automatically in the Memorized Report List. Then, when you want to create a similar report, you can go to the Memorized Report List to find it.

The steps involved in memorizing a report are

* Click Reports -> Select the specific report you want to memorize

* Click the "Memorize" Button.

* Enter the title under which the specified report is going to be memorized

* By clicking Memorize button, the report will be saved.

* You can view, edit or delete the memorized report by selecting Report -> Memorized Reports.

Adding and deleting accounts using chart of accounts

Chart of accounts is the list of predefined account names that a company has identified and that is made available for recording transactions. Chart of accounts may be of different kinds. It may be as large or as complex as the company itself. For example if we look international corporation with several divisions may need thousands of accounts, whereas a small organization could manage in few hundred accounts.

In Numia, the common accounts used across the world for small and large businesses have been listed in Default accounts. In case if you find that your accounts is not listed in default accounts, you can add new accounts. If you need more accounts or sub accounts other than the 'Default accounts', then you can create your own accounts by clicking 'Add new' Button at the page. Just follow these steps to add new account type or account name.

Adding Accounts :

- Go to Banking menu and then select Chart of Accounts.

- Now you can view the list of default accounts and user created accounts.

- If you have not created any accounts then only defaults accounts are listed.

- Click the “Add New” button to add new account type and account name.

- Fill the details like account no, account section, description then click Add Type button.

- Now you new account type is created. You can view the newly created account type in the chart of accounts main page.

- You could also have the provision of editing your user created account types. Just click the edit button in the Chart of accounts page. Then you can change the account type of the existing accounts. But you can't edit the default accounts.

Deleting Accounts :

It is possible to delete your existing accounts in Numia. In “Chart of accounts” page the default accounts and the user created accounts are listed. Just click the delete button corresponding to the account type you need to delete. But once you deleted the account, it is not possible to recover it or view it.

Reversing of Transactions

When a transaction has been entered incorrectly by mistake or accidently, You may need to reverse the transaction. Reversing a transaction means turning the transaction and make it’s effect to zero in the financial records. This process of reversing the transaction is the matter of reversing the debits and credits within the transaction.

When the transaction is reversed, the system will create a new transaction that simply reverses the original transaction debits and credits. In Numia, the Online accounting software, Reversing the transaction can be done by following the steps below.

• Choose Report -> Transaction List.

• Select the transaction that need to be reversed.

• Click on the “Reverse” Button to reverse the transaction.

When the transaction is reversed, the system will create a new transaction that simply reverses the original transaction debits and credits. In Numia, the Online accounting software, Reversing the transaction can be done by following the steps below.

• Choose Report -> Transaction List.

• Select the transaction that need to be reversed.

• Click on the “Reverse” Button to reverse the transaction.

Editing and Deleting of Full and Partial Payments

Many sellers allow the buyers to pay for the product or service both in terms of full payment or partial payment. They make the buyers to pay in installments ie partial payment when he cannot pay the full amount. Partial payment is nothing but the payment that is less than the due amount.

Numia, the online accounting software provides a simple way to record partial payments from your customers. The steps involved in recording partial payments are

• Select Customer -> Receive Payments.

• Choose the customer from which the partial payment is received.

• Select the Payment mode from either cash, cheque or credit card.

• To deposit the payment amount to any of the bank, choose the bank in the “Deposit the amount to field”

• To keep the "Cash In Hand", don't select any option.

• If you want to keep the cash in a fund to deposit later, select Group with Undeposited Funds.

• Choose the invoice for which you have received the partial payment.

• Enter the partial amount paid in the Amount Paid field.

• Click Submit to record partial payment from the customer.

Now, in Numia, you can easily edit, delete the partial and full payments on customer and vendor transactions and do a complete edit / delete of any reconciled / un-reconciled transactions. This can be done by selecting “Reports -> Transaction List”. In the transaction list, just select the transaction to which change has to be done. You will be redirected to the form. Now you can edit and after clicking “Save changes”, your changes has been saved. Numia will automatically add to the credit if you change the amount. You can also delete the transaction by clicking “Delete”.

Numia, the online accounting software provides a simple way to record partial payments from your customers. The steps involved in recording partial payments are

• Select Customer -> Receive Payments.

• Choose the customer from which the partial payment is received.

• Select the Payment mode from either cash, cheque or credit card.

• To deposit the payment amount to any of the bank, choose the bank in the “Deposit the amount to field”

• To keep the "Cash In Hand", don't select any option.

• If you want to keep the cash in a fund to deposit later, select Group with Undeposited Funds.

• Choose the invoice for which you have received the partial payment.

• Enter the partial amount paid in the Amount Paid field.

• Click Submit to record partial payment from the customer.

Now, in Numia, you can easily edit, delete the partial and full payments on customer and vendor transactions and do a complete edit / delete of any reconciled / un-reconciled transactions. This can be done by selecting “Reports -> Transaction List”. In the transaction list, just select the transaction to which change has to be done. You will be redirected to the form. Now you can edit and after clicking “Save changes”, your changes has been saved. Numia will automatically add to the credit if you change the amount. You can also delete the transaction by clicking “Delete”.

Hewlett Packard CEO Mark Hurd- False Expense Report

Right now, most of the medias is covering the news about Mark Hurd, CEO of Hewlett Packard's resignation. Mark Hurd, CEO of HP, following a sexual harrasment investigation has admitted he had a "close personal relationship" with a former marketing contractor.

HP said that althorugh there was no violation of its sexual harassment policy, Mard Hurd violated the company's standards of business conduct by submitting inaccurate expense reports that covered his relationship with the contractor.

HP further claims that Mark Hurd had "...failed to disclose a close personal relationship he had with the contractor that constituted a conflict of interest, failed to maintain accurate expense reports, and misused company assets. Each of these constituted a violation of HP's Standards of Business Conduct..."

It is evidenced that HP has a strong corporate governance that guide / regulate the behaviour of its mangement, employees, or every single on within the firm.

HP said that althorugh there was no violation of its sexual harassment policy, Mard Hurd violated the company's standards of business conduct by submitting inaccurate expense reports that covered his relationship with the contractor.

HP further claims that Mark Hurd had "...failed to disclose a close personal relationship he had with the contractor that constituted a conflict of interest, failed to maintain accurate expense reports, and misused company assets. Each of these constituted a violation of HP's Standards of Business Conduct..."

It is evidenced that HP has a strong corporate governance that guide / regulate the behaviour of its mangement, employees, or every single on within the firm.

#92- Auditing Creditors

One of the procedures required to audit trade creditors account is to audit the creditors' statement received from the audit client's suppliers (i.e. external audit evidence).

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

In normal business circumstances, suppliers will send their monthly Statement of Account to their customers to inform the customers in relation to the outstanding balances. Hence, our audit client will , most likely, receive statement of account from the suppliers.

As part of audit procedure, we can check the suppliers' statement (received by our audit customers) against the creditors' balance recorded in their book. Discrepancies need to be investigated. Statement of account served as an external confirmation to check if our audit client's book has been prepared properly.

However, there are suppliers who do not have practices of sending out Statement of Account to their customers. In this instance, we can send external audit confirmation to the suppliers to confirm outstanding balances.

Deciding Between Bookkeeping Software and Bookkeeping Service

Bookkeeping - the record of day to day financial transactions such as sales, purchase, income and payments by an individual or an organization. These records needed to be produced at the end of every financial year. From small to medium to large business, maintaining financial records is a mush which therefore necessitates bookkeeping process.

The choice of preparing and producing the accounts: organization basically have three options: one is to prepare and maintain records manually; next can be to employ the bookkeeping services and the last option is to use bookkeeping software system.Each has its own advantages and disadvantages. What ever may be the employed method, the ultimate thing is to produce accurate accounting information needed on time.

As the recorded financial transaction is very important for financial decisions and knowledge over the business performance, efficiency and accuracy over the recorded transactions becomes the major concern. Further, the accounting information is the accumulation of documents such as sales invoices, purchase invoices and possibly bank records during the financial year and after the end of the financial year for tax purposes.

Improper records of the above said data (as financial records) leads to unwanted penalties, simply administrative burdens. In analyzing the choices: keeping and maintaining manually may lead to data lose, inaccuracies, fines and penalties thus leading to severe issues at the end of the financial year.

Manual bookkeeping needs regular and periodic evaluation of the data. In going for the choice of having a bookkeeper, trust and knowledge over the operation becomes the mandatory thing for any organization. Also periodic and regular tracking of the works and records maintained is necessary. Having bookkeeper, it is also partially includes in manual work where accuracy level is still depends on the knowledge of the bookkeeper.

The third choice of installing bookkeeping software also has few disadvantages. But these are overruled by its wide advantages. The major advantage is the reduction in paper work and 90% of reducing the manual work thereby achieving accuracy and efficiency. By having bookkeeping software, no one other than the business owners and the authorized person know the financial status which can be called as the security over the accounts.

So by having the gist in hand, the advantages and disadvantages over the choices can be analyzed as discussed above. It can be said with proof that accounting software provides better financial control and performance over the others: manual bookkeeping and having bookkeeper. Thereby administrative burden can be reduced and the organization can focus on its core activities.

How your bookkeeping can boost your tax deductions

Bookkeeping is the key way to bring one’s tax strategy in full circle. It’s the best way to know what is deductible and how to maximize your business deductions. Here is a checklist that make sure bookkeeping is maximizing travel, meals and entertainment deductions. Since these are the three ways where everyone doesn’t have restrictions to themselves. Everyone have to consider these 3 things as major constraints in bookkeeping in order to boost your tax deductions.

Get reimbursed for business expenses that you pay for personally.

Have you ever been to a restaurant that only takes cash? Or traveled in taxi that only accepts cash? Or have you misplaced your business credit card and had to use your personal credit card? These are just some examples where we have to pay our business expenses with personal funds. We could easily miss these expenses so keep an file handy and put all of your receipts in that file. So that you have got a handy report that you have spent from your personal fund.

Have separate account for code meals that are 50% deductible in order to keep them distinct from other expenses that are not subject to this 50% rule. Many times we could see just one meal account in the chart of accounts. The problem with this is that while meals are generally only 50% deductible, some meals are 100% deductible. The mistake that we see most often when reviewing a prospect's prior year tax return, is all meals are treated as only 50% deductible (because they are all coded to one account) and we don’t have any strategy to identify meals that are 100% deductible.

Always maintain your travel expenses separately from your meals and entertainment expenses. As business travel is 100% deductible so separate it out as part of your bookkeeping system. Otherwise, you will have to sort through that account at the end of the year, or worse, you may sometimes forget to sort through that account and everything in the account is treated as only 50% deductible!

Use a separate section in your online bookkeeping software to make notes about who, what, when, where, how much and the business purpose of your travel, meals and entertainment expenses. By proper bookkeeping it is easy to boost your tax deductions, particularly for travel, meals and entertainment. This is an area where deductions are regularly missed and not properly documented, but once you know the rules and use my system, you'll find more and more deductions.

Get reimbursed for business expenses that you pay for personally.

Have you ever been to a restaurant that only takes cash? Or traveled in taxi that only accepts cash? Or have you misplaced your business credit card and had to use your personal credit card? These are just some examples where we have to pay our business expenses with personal funds. We could easily miss these expenses so keep an file handy and put all of your receipts in that file. So that you have got a handy report that you have spent from your personal fund.

Have separate account for code meals that are 50% deductible in order to keep them distinct from other expenses that are not subject to this 50% rule. Many times we could see just one meal account in the chart of accounts. The problem with this is that while meals are generally only 50% deductible, some meals are 100% deductible. The mistake that we see most often when reviewing a prospect's prior year tax return, is all meals are treated as only 50% deductible (because they are all coded to one account) and we don’t have any strategy to identify meals that are 100% deductible.

Always maintain your travel expenses separately from your meals and entertainment expenses. As business travel is 100% deductible so separate it out as part of your bookkeeping system. Otherwise, you will have to sort through that account at the end of the year, or worse, you may sometimes forget to sort through that account and everything in the account is treated as only 50% deductible!

Use a separate section in your online bookkeeping software to make notes about who, what, when, where, how much and the business purpose of your travel, meals and entertainment expenses. By proper bookkeeping it is easy to boost your tax deductions, particularly for travel, meals and entertainment. This is an area where deductions are regularly missed and not properly documented, but once you know the rules and use my system, you'll find more and more deductions.

#91- No depreciation charge on asset held for sale

This is to confirm that if a property is classified as asset held for sale, no depreciation is to be recorded.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

To illustrate, Company ABC entered into Sales & Purchase agreement with 3rd party to dispose one of its property. The Sales & Purchase agreement may take months to complete. In this instance, Company ABC re-classified the property from Property, Plant & Equipment to Asset held for Sale upon entering the Sales & Purchase agreement.

Asset held for sale is de-recognised from the balance sheet upon the completion of the Sales & Purchase agreement.

#90- Review of Credit Term

One of the audit procedures to be performed while reviewing trade debtors balance is to review the credit term given to the customers (i.e. debtors).

To illustrate, we can obtain list of trade debtors, including: credit term given to respective trade debtors, and compare the credit term given to the norm of the industry. We would inquire our audit clients, if credit terms given are unusually long.

For instance, the norm of the credit term in industry A is 90 days. ABC company ( our audit client) allows a credit term of 180 days to customer XYZ. We will have to find out the underlying business reason of giving relatively longer credit term, and evaluate the collectibility of amount owing from customer XYZ.

Analyzing credit term given can be used as a useful tool in understanding the credit policy of our audit client.

To illustrate, we can obtain list of trade debtors, including: credit term given to respective trade debtors, and compare the credit term given to the norm of the industry. We would inquire our audit clients, if credit terms given are unusually long.

For instance, the norm of the credit term in industry A is 90 days. ABC company ( our audit client) allows a credit term of 180 days to customer XYZ. We will have to find out the underlying business reason of giving relatively longer credit term, and evaluate the collectibility of amount owing from customer XYZ.

Analyzing credit term given can be used as a useful tool in understanding the credit policy of our audit client.

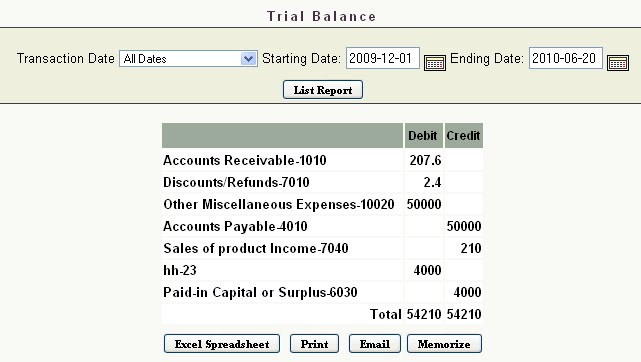

Reporting Trial Balances in Numia

Trial balance is the bookkeeping worksheet in which the balances of all ledgers are compiled into debit and credit columns. A company prepares a trial balance periodically, usually at the end of every reporting period. The general purpose of producing a trial balance is to ensure the entries in a company's bookkeeping system are mathematically correct. The trial balance has three columns. They are name of the ledger account, Credit amount and Debit amount.

The main objectives for preparing trial balance are

• To check arithmetic accuracy.

• To help in preparing Financial statements.

• Helps in locating errors.

• Helps in comparison

• Helps in making adjustments.

In Numia, Online accounting software, You can get the trial balance report easily, showing the debit and credit balances of each account in the chart of accounts. The screenshot for trial balance report in Numia is shown below:

The steps involved are as follows.

• Choose Reports-->Reports review-->Trial Balance.

• The report shows the credit and debit balances for each account.

• You can restrict the report details by selecting dates.

• You can either print the report using print option or export the report to Microsoft excel sheet. You can also able to email it or memorize.

The main objectives for preparing trial balance are

• To check arithmetic accuracy.

• To help in preparing Financial statements.

• Helps in locating errors.

• Helps in comparison

• Helps in making adjustments.

In Numia, Online accounting software, You can get the trial balance report easily, showing the debit and credit balances of each account in the chart of accounts. The screenshot for trial balance report in Numia is shown below:

The steps involved are as follows.

• Choose Reports-->Reports review-->Trial Balance.

• The report shows the credit and debit balances for each account.

• You can restrict the report details by selecting dates.

• You can either print the report using print option or export the report to Microsoft excel sheet. You can also able to email it or memorize.

Payroll Accounting in Numia

Payroll is the sum of all financial records of salaries, wages, bonuses and deductions. In accounting, payroll refers to the amount paid to employees for services, they provided during a certain period of time. Payroll accounting is profitable as you manage and balance small and medium sized businesses.

Online Accounting software, Numia provides you an easier way to calculate and to keep track of the payroll informations of your employees. Add your employee details by entering the required informations. Once you have added the pay tax, pay schedule and deductions of your company, you can easily add payroll for each and every employee. The Screenshot in Numia for adding payroll is shown below:

It can be done by following these steps.

• Choose Add Payroll from the Employee menu.

• Choose the pay schedule for the employee.

• Select the Employee name and enter the rate and quantity for the payroll.

• The net pay will be calculated automatically.

• Click “Add Payroll” to save the payroll created for that employee.

You can also create paychecks for each employee by selecting bank name, account name and entering the check number.

Online Accounting software, Numia provides you an easier way to calculate and to keep track of the payroll informations of your employees. Add your employee details by entering the required informations. Once you have added the pay tax, pay schedule and deductions of your company, you can easily add payroll for each and every employee. The Screenshot in Numia for adding payroll is shown below:

It can be done by following these steps.

• Choose Add Payroll from the Employee menu.

• Choose the pay schedule for the employee.

• Select the Employee name and enter the rate and quantity for the payroll.

• The net pay will be calculated automatically.

• Click “Add Payroll” to save the payroll created for that employee.

You can also create paychecks for each employee by selecting bank name, account name and entering the check number.

#89- Accounting treatment for tax penalty

One of our Accounting & Audiitng blog reader inquired us the following:

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

" How should penalty on late repayment for tax been accounted for?"

Should it be a tax expense? Should it be other expenses?

To clarify: penalty imposed by inland revenue authority on late repayment for tax should not be accounted for as tax expense; it should be accounted for as administrative expense/ other expense.

#88 PWC Singapore issued Disclaimer Audit Opinion for Rickmers Maritime

Recently, PWC Singapore issued Disclaimer Audit Opinion for its client, Rickmers Maritime in view of the Group's uncertainties to continue as a going concern enity.